2025 Q3 Credit Market Update

- Chris Sweet, Managing Director | Head of Capital Advisory

- Scott Thomas, Senior Director

- John Stine, Director

EXECUTIVE SUMMARY

Following tariff-driven disruptions in Q2 2025, credit market activity rebounded in Q3 2025 with primary syndicated loan activity reaching $404 billion – the highest quarterly total on record. Opportunistic refinancing, repricings and dividend recapitalizations continue to dominate issuance activity, but lenders remain extremely supportive of mergers and acquisitions (M&A) given relative lack of M&A financing opportunities. Limited net supply and robust investor demand for loan assets drives significant technical imbalance, resulting in borrower-friendly conditions characterized by flexible terms and credit spreads at or near record lows. Increased competition between the leveraged loan market and the private credit market has also contributed to significantly tighter spreads and more flexible terms in direct lending transactions.

The current environment presents significant opportunities for borrowers to optimize capital structures through refinancing, extended maturities and reduced interest expense. Companies with strong operational performance and clear growth strategies are well-positioned to access favorable financing terms across both the syndicated loan and private credit markets. While M&A activity remains below historical averages, mounting pressure for sponsors to exit investments may drive increased 2026 transaction activity.

Leveraged Loan Issuance Activity

- Despite tariff-related slowdowns in Q2, 2025 leveraged loan issuance volume is currently on pace to be the busiest year since 2021 at $563 billion year-to-date – a nearly 6% increase from the same 2024 period

- Primary syndicated loan activity reached $404 billion in Q3 2025, the highest quarterly total on record. LBO and other M&A-related financing activity accounted for only $36 billion of issuance, the lowest quarterly total this year

- Refinancing issuance surged as borrowers rushed to address 2028 maturities, with B-minus rated borrowers driving 44% of activity

- Speculative-grade borrowers repriced $227 billion of institutional term loans in Q3 2025 – the second-highest quarterly total on record behind Q4 2024 ($279 billion) – driven by a record July ($159 billion)

- Despite record overall activity levels in Q3 2025, new issuance activity remains muted with only 18% of issuance activity tied to new-money transactions

-

- Constrained exit conditions, macroeconomic uncertainty and elevated base rates continue to curb private equity (PE) M&A activity

- Opportunistic deals including repricings, dividend recaps and maturity extensions continue to dominate given muted M&A and record low credit spreads

- PE sponsors financed approximately $35 billion of dividend recaps through the leveraged loan market year-to-date – the highest level in at least seven years

- More than $62 billion dividends financed via the leveraged loan market year-to-date compared to approximately $67 billion for full year 2024, marking the two busiest years on record for leveraged loan dividend recaps

EXHIBIT 1 – Leveraged Loan Issuance Volume

($ in billions)

Source – Pitchbook

EXHIBIT 2 – Total Leveraged Loan Activity by Use of Proceeds

($ in billions)

Source – Pitchbook

Pricing Trends – BSL and Direct Lending Market

- Limited net supply combined with robust investor demand for loan assets is driving a significant technical imbalance, resulting in borrower-friendly conditions

- Credit spreads at or near record lows and flexible terms are supporting opportunistic refinancings, repricings, amendments and dividend recaps

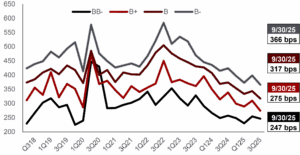

- New-issue spreads for B-minus loans fell to S+366 bps in Q3 – a 58 bps decline year-over-year and the lowest level recorded since the Global Financial Crisis (GFC)

- Spreads for B-rated loans tightened by approximately 60 bps to S+317 bps over the past year marking a decade-plus low. B-plus and BB-minus averages dipped to S+275 bps and S+247 bps, respectively

- Leveraged loan investors executed $441 billion of amendments year-to-date, reducing spreads by 50 bps on average and generating $2.3 billion in annual interest savings

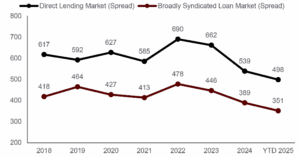

- Increased competition between the leveraged loan and private credit markets has contributed to significantly tighter direct lending transaction spreads

- Average spreads for LBO transactions funded via the direct lending market have fallen below 500 bps year-to-date, more than 160 bps tighter than in 2023

- Market participants report S+450 and S+475 spreads are now common. 56% of direct loans tracked by the LCD were priced below S+500 in Q3 2025, up significantly from 37% in Q2 2025 and 28% in Q3 2024.

- Delta between BSL market and direct lending market spreads reached 147 bps year-to-date, the tightest since 2019

EXHIBIT 3 – Pricing Trends by Rating

(bps)

Source – Pitchbook

EXHIBIT 4 – LBO Pricing trends – Private Credit vs. BSL Market

($ in billions)

Source – Pitchbook

PRIVATE CREDIT

- Private credit became a nearly $2 trillion asset class in recent years as direct lending strategies attracted investors seeking higher yield and risk adjusted returns

- Beyond competing with the syndicated loan market for larger assets, private credit continues to attract middle market and lower middle market borrowers seeking increased flexibility compared with available bank market financing solutions

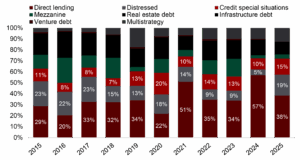

- Private credit fundraising shifted away from direct lending strategies in 2025, favoring special situations and distressed lending as investors seek to deploy higher returning capital in the current environment

-

- Severe technical imbalance from lower-than-expected deal flow contributed to increased competition and lower spreads as demand outpaces supply

- Private credit lenders face challenges maintaining loan portfolio sizes amidst relative lack of large buyouts and increasing private credit loan repayments

- New investments among the 12 largest public BDCs fell by 12% in the first half of 2025 compared to the first half of 2024. Repayments and exits rose by 14%

EXHIBIT 5 – Private Credit Assets Under Management

($ in billions)

Source – Pitchbook

EXHIBIT 6 – Private Credit Capital Raised by Strategy

($ in billions)

Source – Pitchbook

PORTAGE POINT CAPITAL ADVISORY SERVICESPortage Point is a business advisory and investment banking business focused on providing holistic advisory services and solutions to sponsored and non-sponsored middle market companies. The Capital Advisory team partners with clients to evaluate capital requirements, structure tailored financing solutions and run competitive and efficient financing processes to provide certainty of execution and optimize financing outcomes based on unique client goals and priorities. The team leverages years of transaction execution experience and deep lender relationships across the credit provider landscape to develop an effective process strategy and craft thoughtful marketing materials which highlight attractive credit attributes of the business while addressing key lender concerns. In the constantly evolving private credit and middle market financing landscape, middle market companies, financial sponsors and management teams require an experienced and trusted advisor to navigate this marketplace and secure the financing required to fund business objectives. The Portage Point differentiated, cross-functional platform enables the firm to add value for clients across a range of capabilities and solutions prior to, during and after a financing transaction, including financial and operational due diligence, transaction execution services, performance improvement initiatives and value creation and capture initiatives. Contact us to learn how we can positively impact your business. |

Footnotes

1. Non-Refinancing Issuance includes M&A-related financing

Investing in securities involves risk, including the potential loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount originally invested. Past performance is not indicative of future results. All investments carry some degree of risk, including the potential for loss of principal.

Private credit typically refers to debt investments in privately negotiated loans or debt securities. Private credit offers potential benefits such as higher yields, customization of terms, and a focus on steady income generation, but it comes with drawbacks like illiquidity and higher credit risk due to the nature of borrowers involved.

In contrast, broadly syndicated loans are large loans provided by a group of lenders to a single borrower. Broadly syndicated loans are typically rated and have standardized terms, making them more transparent and easier to benchmark. However, they may offer lower yields and less flexibility in terms compared to private credit.

Investing in debt securities is not suitable for all investors. Economic downturns, changes in interest rates, and complex contractual terms further contribute to the risk profile of investing in debt. It is important to conduct thorough research and consider your risk tolerance before making any investment decisions.

This document is for informational purposes only and does not constitute an offer or solicitation to purchase or sell securities. Investors should seek advice from a qualified financial advisor and conduct their own research and due diligence before making any investment decisions.

There is no assurance that any investment strategy will achieve its objectives. All investing involves risk, including the possible loss of principal. Diversification does not guarantee a profit or protect against loss in declining markets.

Investment Banking Services are offered through Triple P Securities, LLC. Member FINRA SIPC. Firm details on FINRAs BrokerCheck.